BIS Says Stablecoins Fall Short On Trust In Money

The Bank for International Settlements says stablecoins can support faster programmable payments, but current designs fall short on core money functions and create risks for financial integrity.

Stablecoins Face A Trust Test

The Bank for International Settlements has put stablecoins at the center of its Annual Economic Report 2026 chapter on digital money, arguing that private tokens show useful payment technology but still fall short of the institutional qualities that make money reliable.

The chapter says digital innovation can make payment systems and financial intermediation more competitive and efficient.

It also warns that the same shift creates macro-financial challenges for central banks and regulators.

Stablecoins are treated as the clearest near-term test because they promise faster and programmable payments while depending on reserve structures, redemption confidence and network acceptance.

BIS does not reject tokenisation as a technology.

Its argument is narrower: programmable ledgers can reduce reconciliation, support direct transfers and allow round-the-clock operations, but money also needs singleness, elasticity, interoperability and financial integrity.

Stablecoins built as private claims do not automatically provide those qualities at system level.

Reserve Design Drives Policy Risk

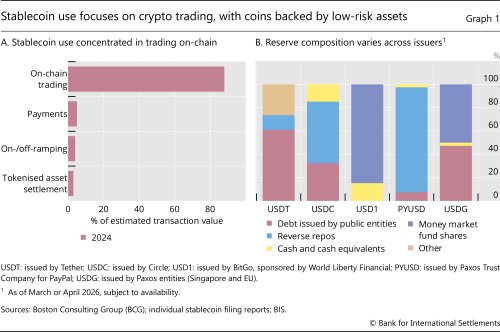

The chapter links stablecoin risk to the composition of issuer reserves and the scale of cross-border demand.

BIS says wider adoption would raise challenges for credit supply, monetary policy, financial stability and fiscal space, even if overall effects on economic activity may remain limited in stylised scenarios.

Redemption pressure is one operational concern.

If stablecoin holders redeem at scale, issuers may need to sell reserve assets or move liquidity quickly, which can affect money markets and funding conditions.

For payment firms and exchanges, the issue is not only whether a token keeps a visible peg during normal trading.

It is whether the backing arrangement can handle stress without pushing risk into the wider financial system.

The chapter also flags stablecoin dollarisation in emerging market and developing economies.

Demand for foreign stablecoins could change capital flows, affect exchange rate dynamics and challenge monetary sovereignty.

That risk gives central banks another reason to improve domestic payment efficiency rather than leave faster digital payments to offshore or foreign-currency tokens.

Central Banks Still Own The Anchor

BIS presents the current monetary system as a two-tier architecture anchored in central bank money and supported by private-sector intermediation.

It says that structure has largely preserved trust, although frictions remain across intermediaries, platforms, competition and cross-border payments.

The chapter's preferred direction is not a return to older payment rails.

It calls for policymakers to tackle weaknesses in current stablecoin arrangements while bringing tokenisation into trusted forms of programmable money.

A unified ledger, or interoperable networks with strong safeguards, could combine tokenised central bank reserves, tokenised commercial bank money, supervised private monies and tokenised assets.

International cooperation is part of that design.

BIS says consistent regulatory approaches can reduce arbitrage and market fragmentation, which matters because stablecoins, reserves and tokenised assets can move across borders faster than domestic rulebooks usually change.

For banks, fintechs and payment processors, the BIS position leaves a clear boundary.

Stablecoins may keep pressure on the market to deliver faster settlement and programmable payment features, but the chapter does not treat private tokens as a complete substitute for public monetary trust.

BIS closes the policy choice around whether regulators can repair stablecoin weaknesses while central banks and commercial banks build programmable money inside supervised rails.