NymCard Pitches a Single Stack for MENA Banks Still Stuck With Patchwork Payment Systems

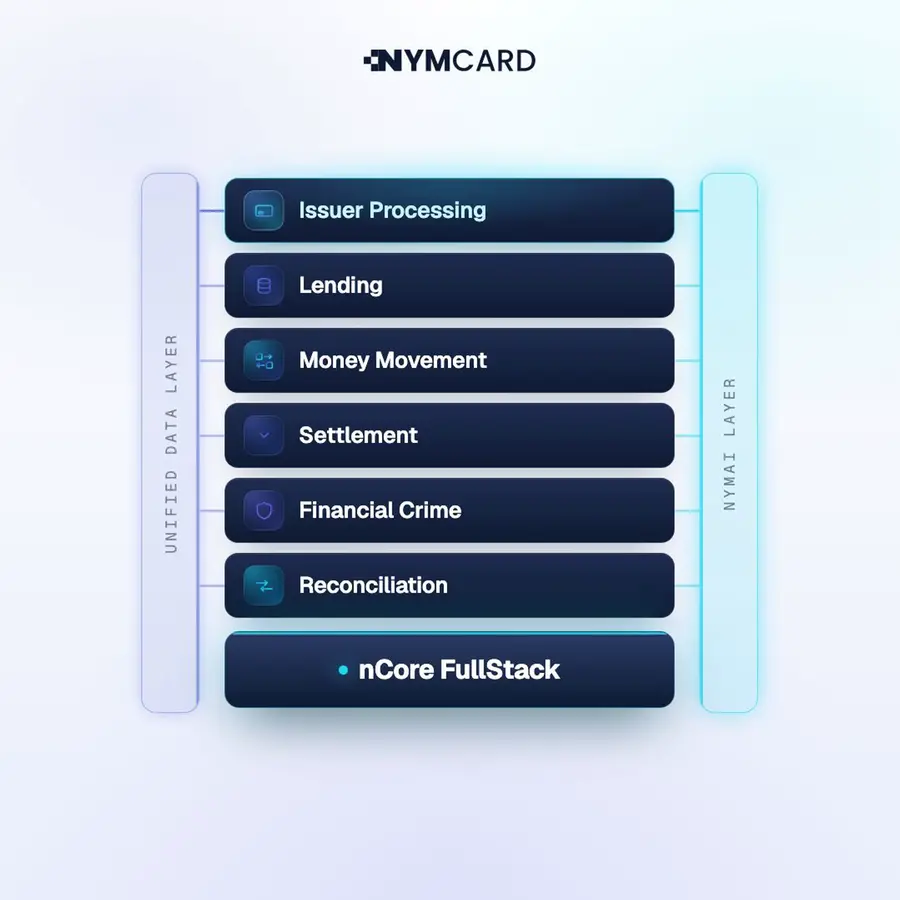

Dubai-based NymCard has launched nCore FullStack, a platform that puts card issuing, lending, money movement, settlement, financial-crime controls and reconciliation behind a single integration. The company says the system can run on public cloud, hybrid, local in-country infrastructure or on-premise deployments, a key point for banks operating under strict regional data-residency rules. NymCard says it powers programmes for more than 60 banks, fintechs and enterprises across eight markets, but the launch still needs to prove that banks will replace fragmented vendor stacks rather than add another layer.

Dubai-based NymCard has launched nCore FullStack, a payments-infrastructure platform aimed at banks that want to add financial products without stitching together a new vendor system each time.

One Integration Across Cards, Lending And Settlement

NymCard says nCore FullStack brings issuing processing, lending, money movement, settlement, financial-crime controls and reconciliation into a single in-house platform.

The company is pitching the product at banks that still run older card-processing systems and add separate tools for payments, fraud, compliance and back-office reconciliation.

The operating pitch is narrower than a broad digital-bank rebrand.

A bank connects to nCore once, then activates capabilities such as card issuing, lending or cross-border payments through the same integration.

NymCard says the bank's core banking system remains the system of record while nCore connects directly to it.

The product list is broad.

The issuing layer covers prepaid, debit, credit, wallet, virtual and tokenized programmes.

The lending layer includes digital onboarding, credit decisioning, loan origination and servicing.

Money movement covers domestic payments, cross-border payments, foreign exchange, remittance and open finance.

Settlement includes fiat, stablecoin and real-time rails, while the financial-crime layer covers card-fraud prevention, anti-money-laundering controls, sanctions screening, identity verification and authentication.

Data Residency Is Part Of The Sales Pitch

For MENA banks, the deployment model is not a side detail.

NymCard says nCore can run on public cloud, hybrid, local in-country infrastructure or on-premise infrastructure, depending on what local regulators require for banking data.

That claim carries extra weight for regional banks.

A modern payments platform that works only in a public-cloud setup can be hard to use where regulators require local hosting, stricter sovereignty controls or direct links into existing core banking systems.

NymCard says the integration remains the same whether a bank chooses on-premise sovereignty or a public-cloud setup.

CEO and founder Omar Onsi framed the product as an answer to banks that keep adding connections on top of ageing infrastructure.

Chief product officer Mario Wehbe said a bank could launch cards first and turn on lending or cross-border payments later without rewriting its core systems.

Chief technology officer Srikanth Achanta said the technical challenge was to keep deployment flexible while keeping the capability set inside one platform.

Migration Is The Hard Part To Prove

NymCard also says banks can move from a legacy processor to nCore without disrupting live programmes.

The company says it uses an agentic AI process and a purpose-built AI engine to move existing card programmes and data onto the platform, and that it has already done this for banks running in production.

Payment-infrastructure decisions are rarely won by feature lists alone.

Banks need to know whether migrations preserve live card programmes, reconciliation records, fraud controls, sanctions workflows and customer-service continuity.

NymCard says the migration process exists; it does not name the production banks or disclose migration volumes, error rates or implementation timelines.

NymCard has some operating scale behind the launch.

The company says it powers payment programmes for more than 60 banks, fintechs and enterprises across eight markets, processes billions of transactions a year and has raised more than $70 million in funding to date.

Cost pressure is also rising.

NymCard cites a forecast that global banks will spend $57 billion on legacy payment-technology maintenance in 2028; the comparable 2022 figure was $36.7 billion.

The Hard Proof Is Bank Adoption, Not Feature Count

The market case is clear enough.

NymCard is trying to replace a fragmented bank-payments stack with one configurable platform that can handle cards, lending, settlement, financial crime and reconciliation under regional deployment rules.

The commercial proof will come from named bank migrations, live product launches on multiple modules and evidence that customers can retire old processors rather than simply connect nCore beside them.

Until those details are public, the launch is best read as a payments-infrastructure bid for banks that want modernization but cannot ignore data residency, core-system integration and operational risk.