Satellite service growth draws more component makers into LEO supply chains

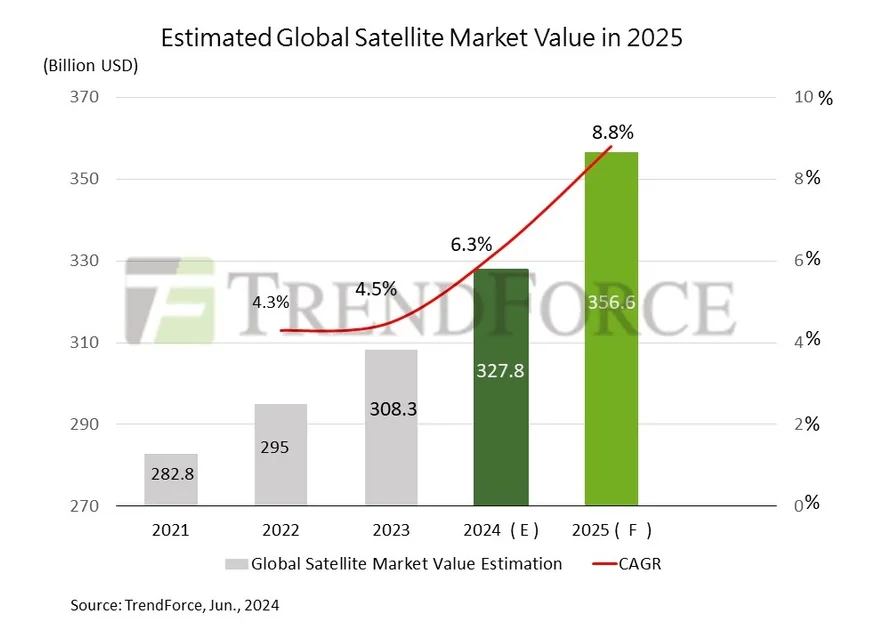

TrendForce said wider adoption of LEO satellite services is pushing component makers toward the supply chains of Starlink and OneWeb. The global satellite market is projected to rise from US$283 billion in 2021 to US$357 billion by 2025, a CAGR of 2.6% (about AED 1,309.69 billion). Starlink relies on vertical integration, while OneWeb uses an outsourced model that broadens participation across suppliers.

Market growth and supply-chain pull

TrendForce said growing use of LEO satellite services is encouraging component manufacturers around the world to join the supply chains of Starlink and OneWeb.

The firm projected that the global satellite market would increase from US$283 billion in 2021 to US$357 billion by 2025, representing a CAGR of 2.6%.

That outlook places the 2025 market at about AED 1,309.69 billion.

The report described how demand growth is affecting the structure of the satellite industry.

Rather than following a single manufacturing template, major LEO suppliers are building their systems with very different sourcing models.

TrendForce highlighted this contrast through Starlink and OneWeb, showing how one company keeps more production in-house while the other depends more heavily on external partners.

Starlink's vertically integrated approach

TrendForce said Starlink currently uses a vertical integration strategy for its supply chain.

It produces and assembles key satellite components at its own factory in Washington, USA.

The components named in the report include payload channel elements, Ka-band antenna elements, filters, and separators.

According to TrendForce, making these parts internally helps Starlink manage production conditions more directly and lowers supply-chain management complexity.

This model gives the company tighter control over critical manufacturing steps and assembly work.

TrendForce also said larger Taiwanese manufacturers that enter Starlink's supply chain usually have the resources and organizational systems needed to satisfy strict space testing requirements.

Examples include random vibration tests and separation shock tests.

Smaller Taiwanese satellite component makers, by contrast, face greater difficulty joining Starlink's supplier network because their resources are more limited.

OneWeb's outsourced supplier network

TrendForce described OneWeb as taking a highly outsourced approach to its supply chain.

The company assigns production of key satellite components to regional Tier 2 parts manufacturers.

After that, subsystem factories complete part of the assembly process before the components are delivered to OneWeb Satellite for final assembly.

This structure creates a more accessible path for outside suppliers than a tightly controlled in-house model.

TrendForce said the approach enables a wider range of component makers to work with OneWeb and supports their move into the LEO satellite sector.

The report presented this as an important distinction between the two companies' supply systems.

TrendForce added that small and medium-sized Taiwanese satellite component manufacturers are expected to seek partnerships with satellite companies that use open supply-chain arrangements such as OneWeb.

This route may offer a more practical entry point for firms that cannot easily meet the demands of a vertically integrated supplier system.

Taiwan-related collaboration efforts

TrendForce said opportunities for cooperation between OneWeb and Taiwanese key component manufacturers are being promoted through government project plans and field verification models.

The report said support from LEO satellite projects can help Taiwanese satellite component makers reduce some of the risks tied to entering an emerging market.

It also said these projects can give manufacturers an initial view of how target markets are accepting LEO satellite services and help them judge how much they may want to invest in the future.

In that context, the spread of satellite services is not only expanding the market's size, but also reshaping who can participate in the supply chain and under what conditions.

Across the market, TrendForce's comparison of Starlink and OneWeb points to two different ways suppliers are being drawn into LEO production: a vertically integrated model centered on internal manufacturing control, and an outsourced model built around regional component and subsystem partners.

Summary version for Medium

Satellite service growth draws more component makers into LEO supply chains

What the announcement means beyond the headline

Quick Summary: TrendForce said wider adoption of LEO satellite services is pushing component makers toward the supply chains of Starlink and OneWeb. The global satellite market is projected to rise from US$283 billion in 2021 to US$357 billion by 2025, a CAGR of 2.6% (about AED 1,309.69 billion).

Market growth and supply-chain pull

TrendForce said growing use of LEO satellite services is encouraging component manufacturers around the world to join the supply chains of Starlink and OneWeb. The firm projected that the global satellite market would increase from US$283 billion in 2021 to US$357 billion by 2025, representing a CAGR of 2.6%.

Starlink's vertically integrated approach

TrendForce said Starlink currently uses a vertical integration strategy for its supply chain.

- Point 1: The central topic is science-tech, with the announcement framed around concrete operating detail.

- Point 2: It produces and assembles key satellite components at its own factory in Washington, USA.

The useful takeaway is the operating constraint behind the announcement, not the announcement alone.

OneWeb's outsourced supplier network

TrendForce described OneWeb as taking a highly outsourced approach to its supply chain. The company assigns production of key satellite components to regional Tier 2 parts manufacturers.

Read the Full Deep Dive

Want to explore the complete technical analysis, enterprise trade-offs, and detailed metrics?

Read the full article originally published at SendTech Times